How We Reduced Merchant Onboarding from 18 to 4 Days

When we were approached by this payment processor, the situation was delicate. The company had just closed a significant growth round and was aggressively expanding its merchant base. The problem was that each new merchant took an average of 18 days to be approved and start processing transactions. For a company competing directly with giants like Stripe and Square, this delay was a critical competitive issue.

The onboarding process involved manual document verification, risk analysis, KYC/AML compliance validation, and approval across multiple layers. The operations team was overloaded, working with spreadsheets, emails, and a legacy system that required manual data entry at virtually every stage. The VP of Operations told us that the industry benchmark was between 3 and 5 days, and some competitors were already managing to approve merchants in 48 hours. The last straw came when one of their main competitors launched an advertising campaign promising onboarding in less than a week. The processor began losing important deals, especially from merchants who needed to start operating quickly. The sales team was frustrated because they could attract good prospects, but many gave up during the approval process or simply went to competitors who promised speed.

Internally, the company had discussed building an in-house solution. The CTO presented a 14-month plan that would require hiring three additional engineers and pausing other critical roadmap projects. The estimated cost was over half a million dollars, not counting the opportunity cost of delaying other initiatives. The board was divided between investing heavily in internal development or finding a faster alternative. It was in this context that we began our analysis. We spent an entire week mapping the complete process, from the moment the merchant filled out the initial form to final approval. We discovered that 73% of the time was spent on tasks that could be automated: extracting data from PDF documents, validating information in public databases, calculating risk scores, and generating compliance reports.

What we proposed was a system we internally called MerchantFlow AI. The architecture was designed to integrate with the company’s existing systems without requiring a complete infrastructure overhaul. We used computer vision to automatically extract data from identity documents, corporate contracts, and bank statements. We built connectors with public databases for automatic validation of tax IDs, sanctions list verification, and fraud history checks.

The most complex part was the risk scoring engine. We worked directly with the company’s risk team to understand the criteria they used manually to evaluate each merchant. We converted these criteria into a machine learning model that could automatically classify merchants into three categories: automatic approval, standard manual review, and in-depth manual review. The model was trained with historical data from 2,400 merchants approved over the previous two years.

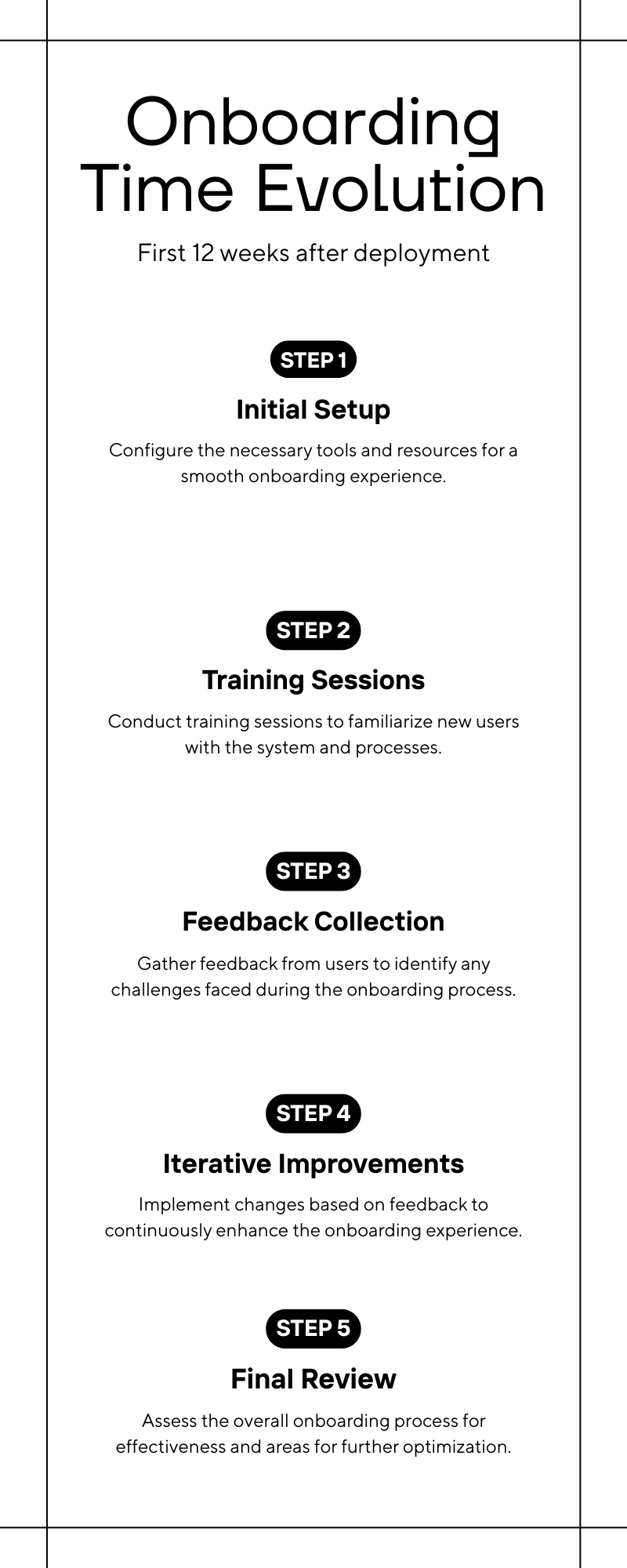

Development took 58 days. We worked in two-week sprints, with regular demos for the operations team. Each sprint, they tested the features, provided feedback, and we adjusted. This iterative approach was crucial because it allowed the team to gradually familiarize themselves with the system and because we captured edge cases that we wouldn’t have identified just by looking at documentation.

The deployment phase was carefully planned. We didn’t want to shut down the old system all at once and risk interrupting operations. For three weeks, we ran both systems in parallel. Every new merchant went through MerchantFlow AI, but the operations team still manually verified using the old process. This served as validation and also as training. When we saw that the system was achieving 94% agreement with human decisions, we made the complete transition.

Results began to appear immediately. In the first week after full go-live, the average onboarding time dropped to 6 days. It seemed good, but was still above target. We made some adjustments to automatic approval thresholds, optimized some slow queries, and added caching to frequent external calls. By the third week, we reached a 4.2-day average. Two months later, we were consistently at 3.8 days.

But the time reduction was only part of the impact. The operations team, which previously spent 80% of their time doing data entry and manual verifications, was reallocated to more strategic functions. Two analysts were moved to the fraud prevention area, where they set up a proactive monitoring program that has already identified three fraud schemes before they caused significant losses. Another analyst began working directly with the sales team, helping to pre-qualify prospects and further accelerate the funnel. The financial impact went beyond operational efficiency. With the new onboarding time, the conversion rate from prospects to active merchants increased by 34%. Merchants who previously gave up mid-process now completed the journey. The sales team began using onboarding time as a sales argument, and this became a real competitive differentiator. The company calculated that the increase in conversion represented $612,000 in additional revenue in the first year.

There was also an unexpected gain in compliance. Since the system automatically documents each step of the verification process, compliance audits that previously took weeks of preparation are now done in days. When the company went through a regulatory audit six months after deployment, the auditors praised the traceability and consistency of the process. This doesn’t have direct financial value, but significantly reduces regulatory risk. The system has been running for just over a year now. The company has processed more than 1,800 onboardings since then. The automatic approval rate is at 67%, which means two-thirds of merchants are approved without any human intervention. The remaining 33% go through review, but even in these cases, the system has already done all the initial collection and verification work, so the analyst only needs to make the final decision.

Recently, the company’s product team used the same MerchantFlow AI infrastructure to build a KYC process for marketplace sub-merchants. They managed to implement this in three weeks because all the computer vision foundation, external data integration, and risk scoring already existed. This type of reuse wasn’t in the original project scope, but demonstrates the value of building well-architected systems.

Looking back, what made this project work was the combination of deep domain knowledge in finance operations with rapid technical execution. We didn’t try to revolutionize the company’s onboarding process. We took what they already did well, automated the repetitive parts, and let humans focus on critical judgment. The result was a system that the team quickly adopted because it made sense to them and because it visibly made their work better.

For Huyawo, this project confirmed something we already suspected: finance operations companies don’t need generic AI. They need systems that deeply understand the nuances of compliance, risk, and regulation in the financial sector. And they need these systems delivered quickly, not in 18-month roadmaps. The difference between 18 and 4 days of onboarding may seem operational, but for a growing company, this is the difference between winning and losing market share.